The Good News

The FHA Single Unit Approval program, formerly known as Spot Approval, allows an FHA mortgage to fund in an association, without the project having to obtain FHA certification. This is great news since FHA approval is a costly and time-consuming process that prevents sellers from accepting an offer from an FHA buyer due to the four weeks it takes to get certified. This new lending program now extends FHA mortgages for buyers and refinancing owners in the 140,000 condominium associations that are not FHA approved.

The Problem

However, there is a problem with the Single Unit Approval program, and it’s the same problem that it existed when it was called Spot Approval from 1996-2010. While the association doesn’t have to obtain FHA approval under this program, it still has to qualify. To know if a particular association qualifies, a thorough review of the governing and legal documents, along with review of the maps and insurances, coupled with an in depth analysis of all financials documents, has to be done by someone competent to render a yes or a no. No real estate agent, loan officer, closing agent, or property manager possesses the required expertise or experience to know whether a given association is eligible. The only person in the process that has this expertise is the lender’s DE underwriter, who reviews the hundreds of pages of documents and says yea or nay three weeks into the transaction. Translation: Not early.

How often?

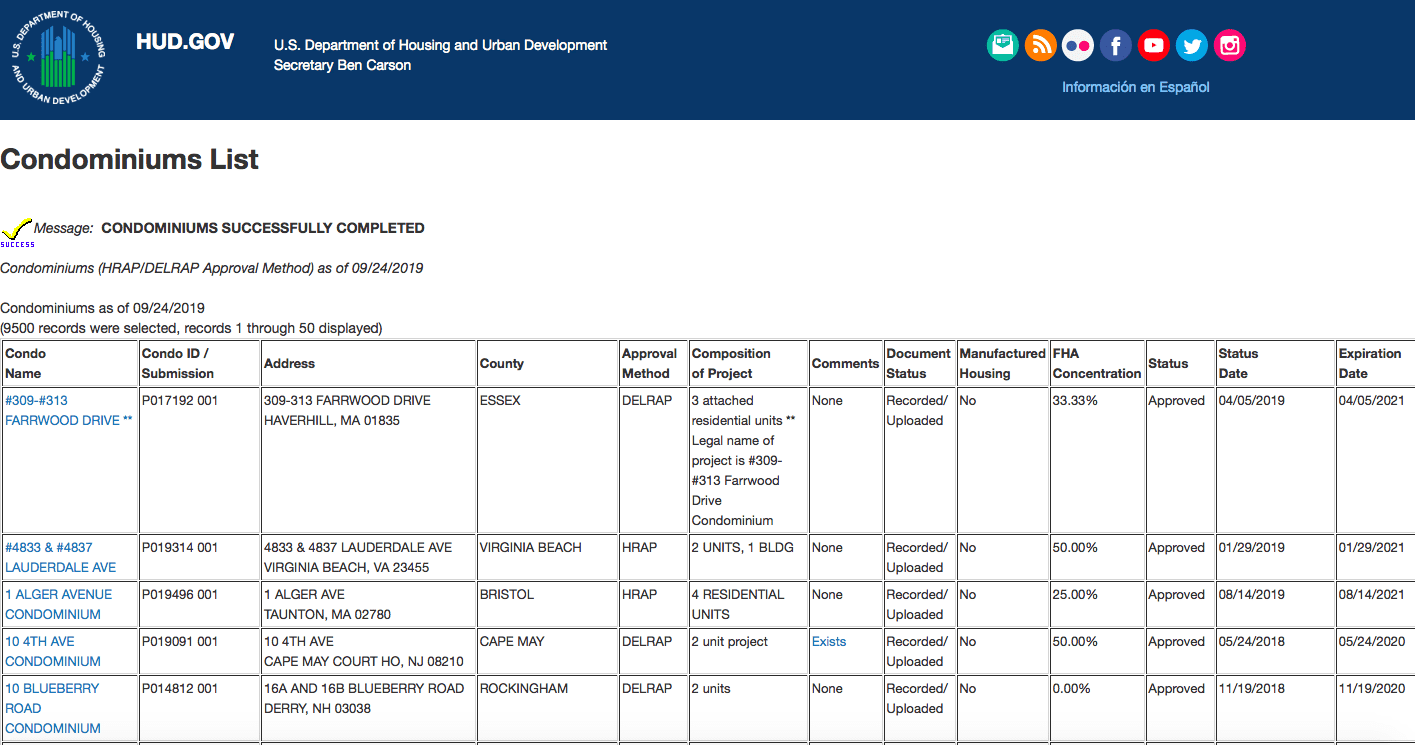

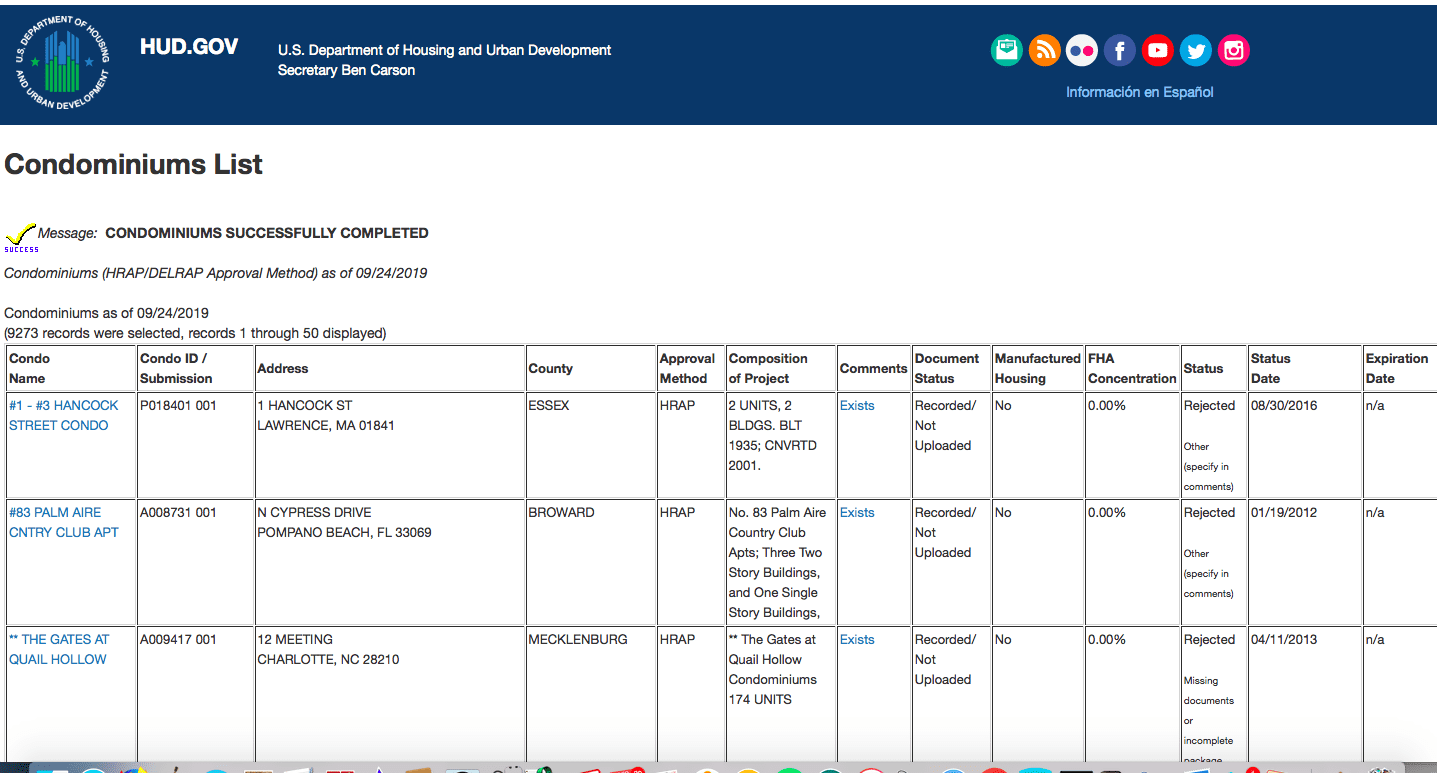

To determine how much of a problem this is, we need to know how often a condominium under Single Unit will be ineligible. Below are two recent screen shots from HUD.gov’s FHA condominium roster, where all condominiums ever submitted to HUD reside.

9500 currently approved condominiums

9273 currently rejected condominiums

Half the time the association under Single Unit will be ineligible, for one of fifty reasons. And this will be discovered three weeks into the transaction.

The Pain

For the fifty percent of the time that the condominium fails, there is plenty of pain to go around. The seller takes their property off the market for three weeks, only to have to relist it for sale, which always hurts the value. The buyer has to start looking again, having spent appraisal and inspection monies that they will never get back. The listing and buyers agents have to go back to work and do it all over again, with no guarantee that either will ever successfully enter into a contract with their client again. If it’s a refinancing owner, he loses his appraisal cost, and if a reverse mortgage, counseling and the cost of various certifications.

The Solution

The solution to the Single Unit dilemma is to order the HOAFAX report as soon as possible. The HOAFAX report, like a Carfax for the condo, reviews all of the association documents and financials immediately against the Single Unit program, and publishes a report with a traffic light icon that establishes whether a Single Unit loan is possible. If ordered by the seller/listing agent when the property is listed, it enables the listing agent to market the property accurately with the HOAFAX report that the unit is or is not definitively eligible for Single Unit purchasers. For the buyer purchasing the unit where the seller has not ordered the HOAFAX, he needs to order it immediately upon going under contract to ensure his inspection and appraisal monies, along with his hope and time, isn’t wasted. So be smart and order the HOAFAX today, and know from the get go.